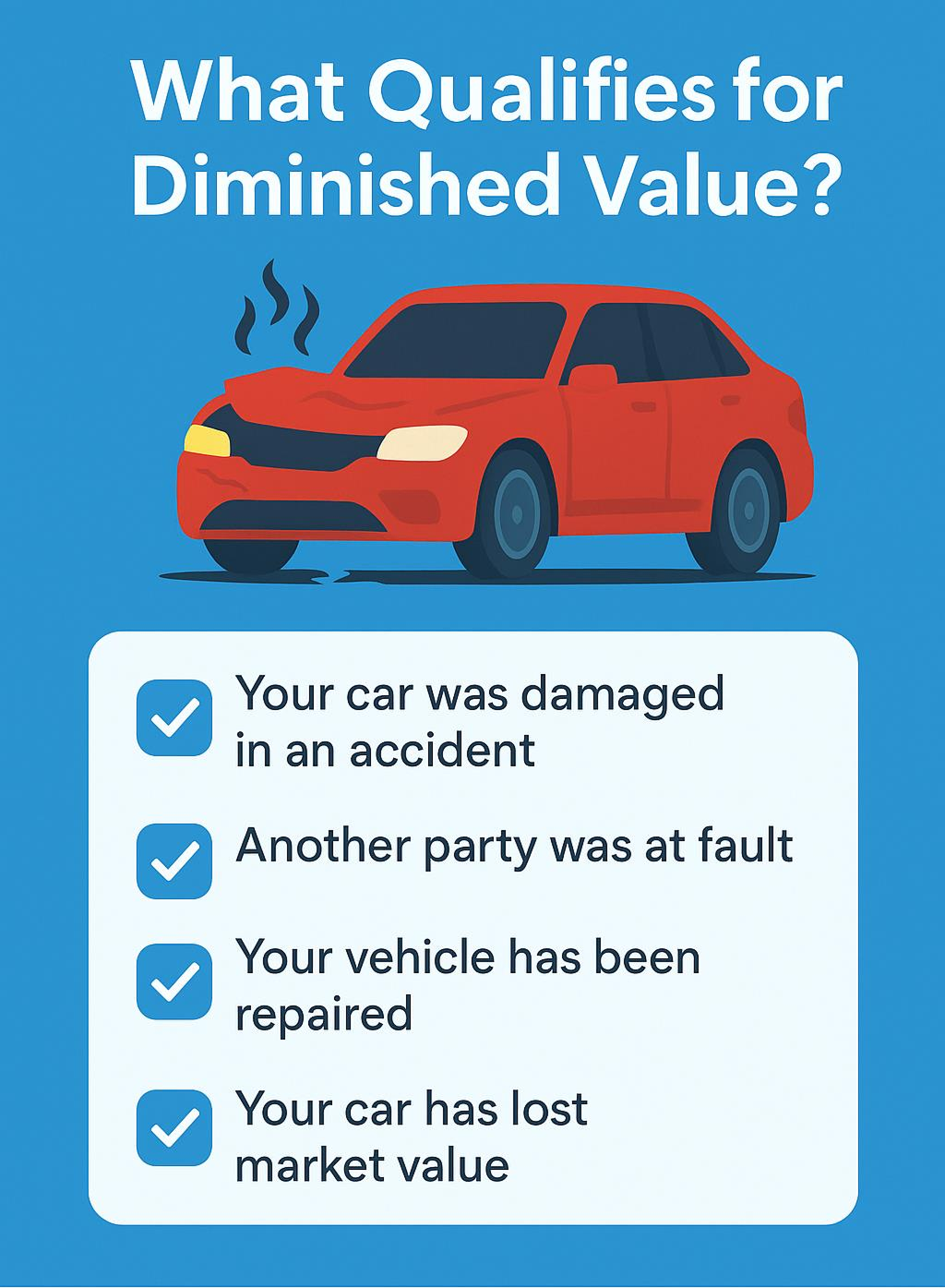

Even if your repair work is perfect, inherent diminished value remains. This is because potential buyers use accident history as a measure of reliability. Cars with an accident record might sell for less, as people think they may bring future problems. Insurance policies usually consider this type of claim, especially when the fault driver is clearly responsible for the crash.

We help drivers recover the money they’re owed after an accident, especially for diminished value claims—no stress, no runaround, just results.